Inheritance taxation can be an important instrument to address inequality, particularly in the current context of persistently high wealth inequality and new pressures on public finances linked to the COVID-19 pandemic, according to a new OECD report.

Inheritance Taxation in OECD Countries provides a comparative assessment of inheritance, estate and gift taxes across the 37-member OECD, and explores the potential role these taxes could play in raising revenues, addressing inequalities and improving the efficiency of tax systems in the future.

The report highlights the high degree of wealth concentration in OECD countries as well as the unequal distribution of wealth transfers, which further reinforces inequality. On average, the inheritances and gifts reported by the wealthiest households (top 20%) are close to 50 times higher than those reported by the poorest households (bottom 20%).

The report points out that inheritance taxes – particularly those that target relatively high levels of wealth transfers – can reduce wealth concentration and enhance equality of opportunity. It also notes that inheritance taxes have generally been found to generate lower efficiency costs than other taxes on the wealthy, and to be easier to assess and collect than other forms of wealth taxation.

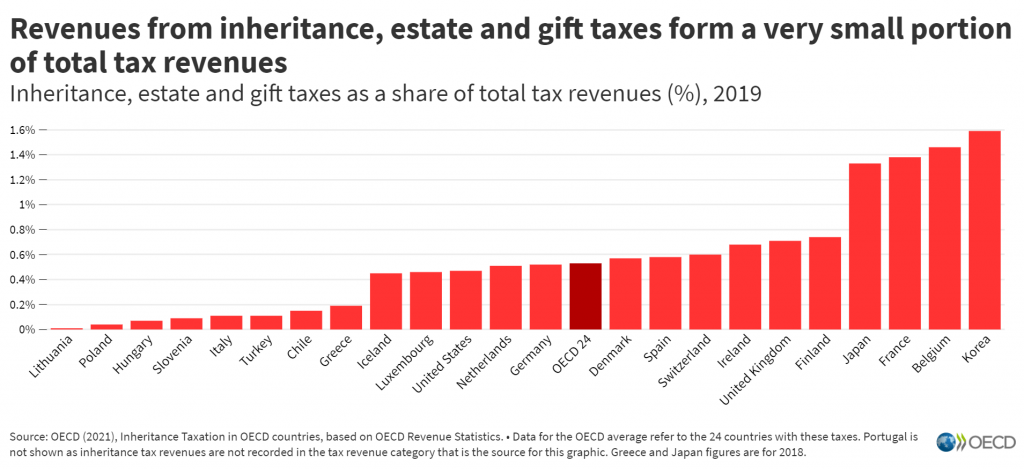

A majority of OECD countries currently levy inheritance or estate taxes – 24 in total. However, these taxes typically raise very little revenue. Today, only 0.5% of total tax revenues are sourced from inheritance, estate and gift taxes on average across the countries that levy them.

Generous tax exemptions and other forms of relief are a key factor limiting revenue from these taxes, according to the report. In addition to limiting revenue, relief provisions primarily benefit the wealthiest households, reducing the effective progressivity of inheritance and estate taxes.

Individuals are often able to pass on significant amounts of wealth tax-free to their close relatives thanks to high tax exemption thresholds. Tax relief is also common for transfers of specific assets (e.g. main residence, business and farm assets, pension assets, and life insurance policies). In a number of countries, inheritance and estate taxes can also largely be avoided through in-life gifts, due to their more favourable tax treatment.

These provisions reduce the number of wealth transfers that are subject to taxation, sometimes significantly so. For instance, across eight countries with available data, the share of estates subject to inheritance taxes was lowest in the United States (0.2%) and the United Kingdom (3.9%) and was highest in Switzerland (12.7%) (Canton of Zurich) and Belgium (48%) (Brussels-Capital region).

“While a majority of OECD countries levy inheritance and estate taxes, they play a more limited role than they could in raising revenue and addressing inequalities, because of the way they have been designed,” said Pascal Saint-Amans, director of the OECD Centre for Tax Policy and Administration. “There are strong arguments for making greater use of inheritance taxes, but better design will be needed if these taxes are to achieve their objectives.”

The report underlines the wide variation in inheritance tax design across countries. The level of wealth that parents can transfer to their children tax-free ranges from close to USD 17 000 in Belgium (Brussels-Capital region) to more than USD 11 million in the United States. Tax rates also differ. While a majority of countries apply progressive tax rates, one-third apply flat rates, and tax rate levels vary widely.

The report proposes a range of reform options to enhance the revenue potential, efficiency and fairness of inheritance, estate and gift taxes, while noting that reforms will depend on country-specific circumstances.

It finds strong fairness arguments in favour of an inheritance tax levied on the value of the assets that beneficiaries receive, with an exemption for low-value inheritances. Levying an inheritance tax on a lifetime basis – on the overall amount of wealth received by beneficiaries over their lifetime through both gifts and inheritances – would be particularly equitable and reduce avoidance opportunities, but could increase administrative and compliance costs. Scaling back regressive tax reliefs, better aligning the tax treatment of gifts and inheritances and preventing avoidance and evasion are also identified as policy priorities.

To make these taxes more acceptable by the public at large, the report underlines the need to provide citizens with information on inequality and the way inheritance and estate taxes work, as these tend to be misunderstood.

“Inheritance taxation is not a silver bullet, however,” said Mr Saint-Amans. “Other reforms, particularly in relation to the taxation of personal capital income and capital gains, are key to ensuring that tax systems help reduce inequality. The OECD will be undertaking new work in that area, in particular as the progress made on international tax transparency and the exchange of information is giving countries a unique opportunity to revisit personal capital taxation.”